What is subprime loans?

A subprime loan is a type of loan that is made out to borrowers with lower credit ratings. In other words, these are borrowers who present a higher risk that the loan won't be repaid.

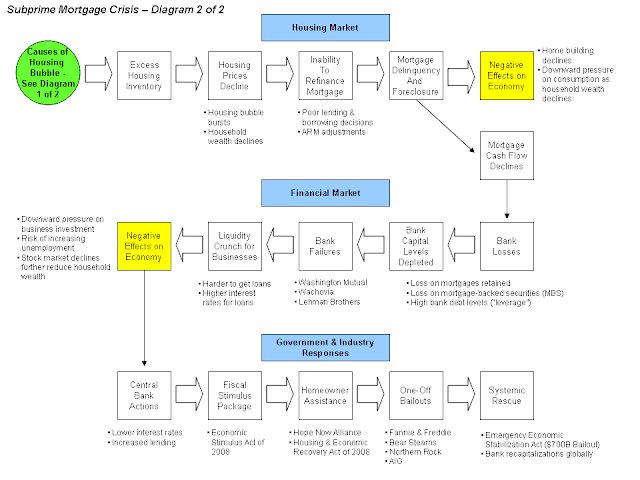

Subprime loans played a significant role in the 2008 financial crisis and the subsequent economic recession. In 2007, the US economy experienced an out-of-control number of mortgage failures leading to unprecedented number of foreclosures. More than half of these foreclosures in the US were as a result of the subprime mortgage loans.

Subprime loans have inherent risks both to the borrower and the lender. To the borrower, subprime loans had the risk that they were adjustable rate mortgages (ARMs). This means that the interest rate would adjust or change overtime. Overtime, the adjusted time interest rate would interest rate become unaffordable to the borrower leading to imminent foreclosure.

To the lender, subprime loans presented a different type of risk. Since the loans were given to borrowers who fell in the risky category, they attracted a higher interest rate which led to nonpayment or increased rates of default. To cover this risk, the lenders sold the mortgage debt to other intermediaries further compounding the problem.

References

Gilbert, J. (2011). Moral Duties in Business and Their Societal Impacts: The Case of the Subprime Lending Mess. Business & Society Review, 116(1), 87-107. doi:10.1111/j.1467-8594.2011.00378.x

Pajarskas, V., & Jočienė, A. (2014). Subprime Mortgage Crisis In The United States In 2007-2008: Causes and Consequences (Part I). Ekonomika / Economics, 93(4), 85.

Ross, L. M., & Squires, G. D. (2011). The Personal Costs of Subprime Lending and the Foreclosure Crisis: A Matter of Trust, Insecurity, and Institutional Deception. Social Science Quarterly (Wiley-Blackwell), 92(1), 140-163. doi:10.1111/j.1540-6237.2011.00761.x